Jordan is a small, open economy in the Middle East with a population of around 11 million and a GDP of roughly USD 50–55 billion (Heritage Foundation, 2025).

The Kingdom has limited natural resources and faces persistent challenges such as high unemployment — around 21-22% in recent years, and a heavy public debt burden. At the same time, it benefits from a well-educated population and a stable political environment (Digital Frontiers Institute, 2019; DOS Jordan).

Economic growth has been modest, averaging between 2-3% annually during the mid-2020s.

Inflation has remained relatively low, under 4%, reflecting prudent monetary policy implemented by the Central Bank of Jordan (IMF, 2024).

These conditions have helped maintain macroeconomic stability despite structural constraints.

The financial sector accounts for about 12% of GDP (DFI, 2019) and plays a vital role in supporting development.

However, traditional banks have been cautious in extending credit to:

- Micro and small enterprises

- Lower-income individuals

This limited outreach has created space for non-bank financial institutions (NBFIs) to step in.

By offering credit to underserved segments, NBFIs have emerged as important drivers of financial inclusion and a complement to the banking sector.

Key Economic Indicators (2024)

¹ Note: Some sources cite 6.50% as the Central Bank of Jordan’s (CBJ) policy benchmark. The difference reflects the use of the repo rate vs. rediscount rate in various reports.

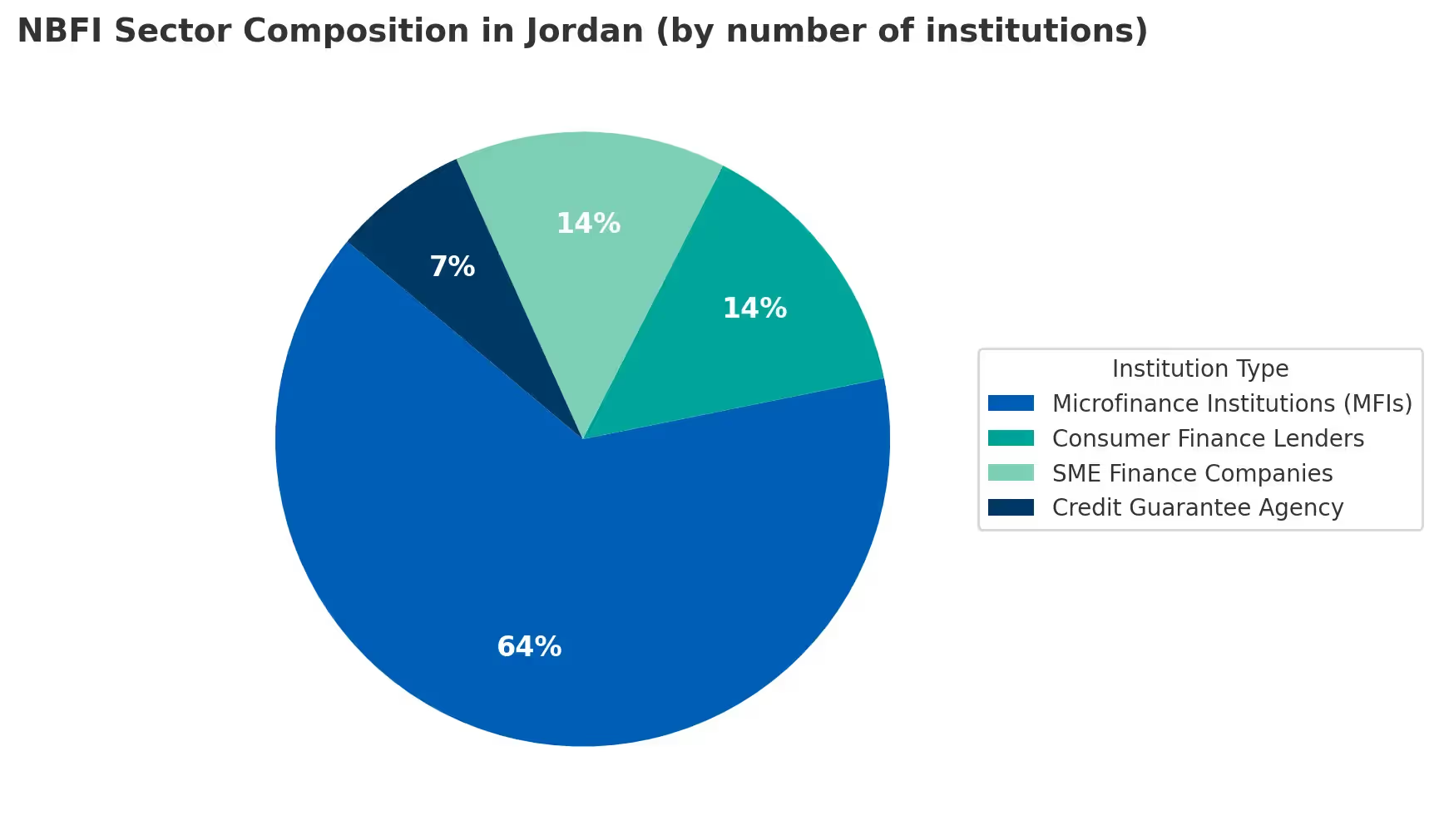

Jordan’s NBFI Sector at a Glance

Non-bank financial institutions (NBFIs) in Jordan consist of finance companies that extend credit outside the deposit-taking banking system.

These include microfinance institutions (MFIs), leasing and factoring companies, consumer lending firms, and emerging fintech lenders.

The Central Bank of Jordan (CBJ) formally regulates them under the Finance Companies Bylaw No. 107 (issued in 2021) (World Bank, 2025).

Unlike banks, NBFIs do not accept customer deposits. Instead, they finance lending activities through equity, debt, or wholesale funding lines.

They focus on serving market niches often overlooked by banks, such as low-income borrowers, micro and small enterprises, consumer finance for the unbanked, and other specialised credit needs.

By 2023, Jordan had nine licensed microfinance companies (established under a 2015 CBJ regulation) and several other finance companies specialising in consumer and SME lending (DFI, 2019).

Collectively, these NBFIs have become an essential part of the financial landscape, complementing the banking sector and advancing national goals for financial inclusion.

Regulatory Integration

The CBJ’s Finance Companies Bylaw No. 107 of 2021 created a unified regulatory framework for NBFIs, bringing finance companies (including MFIs, leasing, and factoring firms) into the formal financial system (World Bank, 2025).

- Licensing requirements: Existing finance companies were granted a grace period until May 2024, later extended to July 2025, to obtain a CBJ license.

- Objectives: The reform aims to bring “shadow” lenders under official oversight, enhancing transparency, consumer protection, and overall sector stability.

- Innovation provisions: Amendments introduced a Regulatory Sandbox to encourage fintech development and a tiered licensing regime for crowdfunding and peer-to-peer lending platforms.

These reforms underscore the regulator’s commitment to fostering NBFI growth, encouraging innovation, and integrating non-bank finance more closely with Jordan’s broader financial system.

Key Players and Market Positioning

Jordan’s NBFI landscape is diverse, ranging from socially oriented microfinance institutions to tech-driven consumer lenders.

Key Players

The table below highlights some of the major NBFIs in Jordan and their focus areas:

Market Positioning

Traditional MFIs (MFW, Tamweelcom, AMC, FINCA Jordan, etc.) focus on microloans of a few hundred to a few thousand dinars, serving ~456,000 borrowers, 70% of whom are women.

Fintechs like MFF and Lendo target consumer finance with fast, small loans.

SME players like Liwwa and Sanadcom bridge the gap for enterprises that are too large for microcredit but are underserved by banks.

Growth Trends in Non-Bank Lending

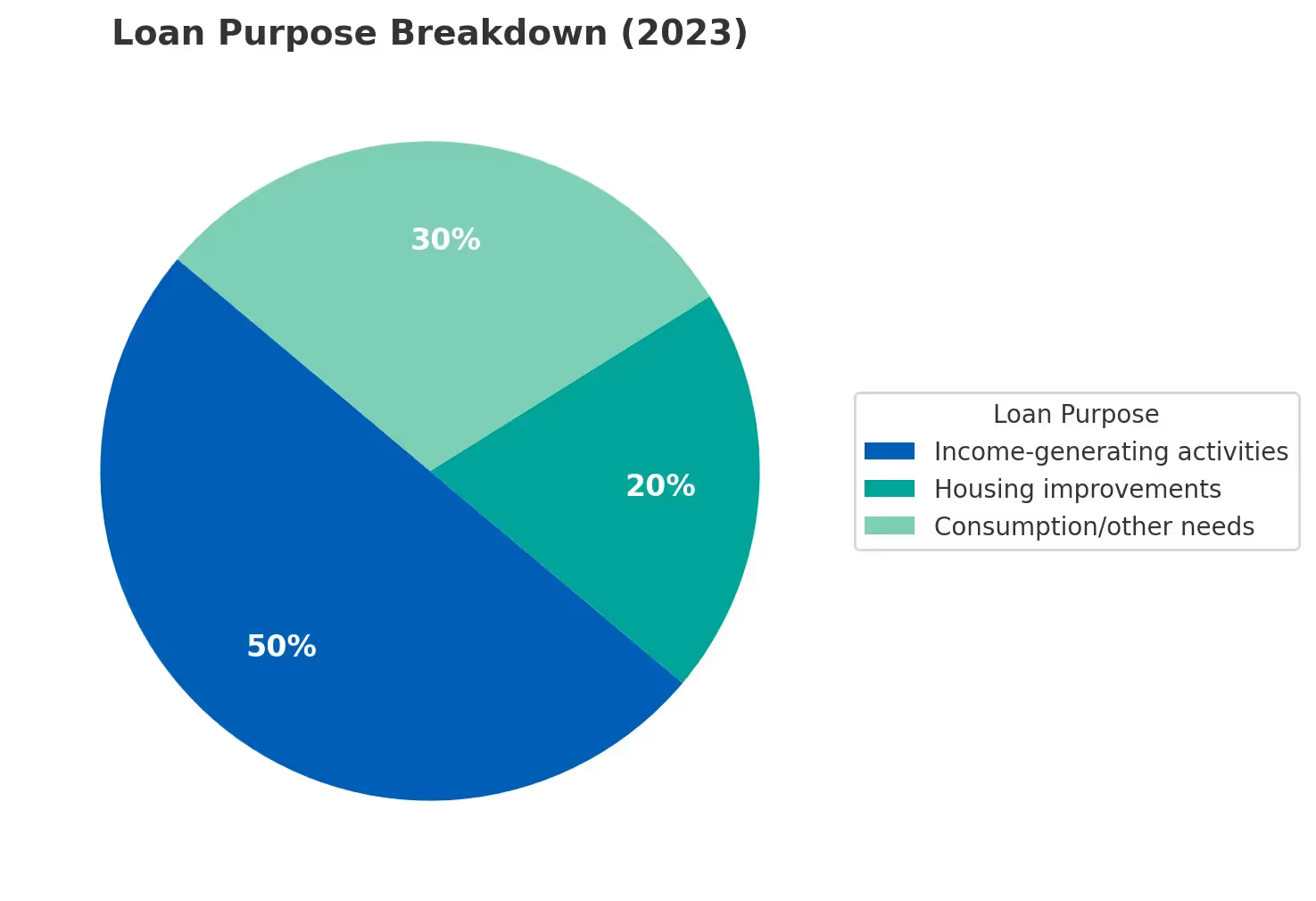

After rapid expansion in the 2010s, Jordan’s non-bank lending sector has continued to grow at a steadier pace. By Q4 2023, total outstanding microfinance loans reached approximately JOD 308 million, up from around JOD 261 million in 2018.

The number of borrowers, about 456,000, remained broadly stable, suggesting that outreach may be reaching saturation. At the same time, average loan sizes increased from roughly JOD 542 in 2018 to JOD 695 in 2023, reflecting either higher financing needs or inflationary adjustments.

Portfolio-at-risk (PAR) greater than 30 days rose from about 3% in 2018 to 4.7% in 2023, indicating some deterioration in asset quality.

Regarding loan purpose, around 50% of microcredit was directed to income-generating activities, 20% to housing improvements, and the remainder to consumption-related needs.

Emergence of Fintech Lenders

Recent years have seen fintech lenders transform Jordan’s non-bank financial sector:

- Money for Finance (MFF): Scaled rapidly to 54 branches by 2024, achieved repeat loan rates above 90%, and was recognised as the “Best Fintech Consumer Lending Company in Jordan.”

- Lendo: Pioneered payday-style lending, building a portfolio of around €2.3 million by 2022.

- Liwwa: Attracted backing from development finance institutions such as the U.S. DFC and FMO, enabling it to channel tens of millions of dollars into SME loans.

These fintech-oriented NBFIs underscore the strong demand for accessible credit in both the consumer and SME segments, and they highlight the sector’s shift toward technology-driven models of financial inclusion.

Key Financial Metrics (Microfinance Sector)

Lending Models Beyond Microfinance

Jordan’s non-bank financial institutions (NBFIs) and fintechs have diversified significantly beyond traditional microloans.

Today, a variety of lending models target consumer, SME, and vehicle financing needs.

Consumer Finance and Short-Term Loans

Fintech lenders have introduced fast, convenient loan products to cover emergencies and small purchases:

- Money for Finance (MFF): Offers quick, small-ticket consumer loans through a mix of digital onboarding and a wide branch network.

- Lendo: Specialises in payday-style loans with rapid approval, designed for short-term liquidity needs.

These models emphasise speed and accessibility, meeting demand from underbanked consumers.

Buy Now, Pay Later (BNPL)

BNPL has gained traction in Jordan, with both regional fintechs and established banks participating:

- AlWasleh: Provides retail instalment plans; expanded via a partnership with Network International.

- ZoodPay: Operates embedded BNPL solutions with both online and offline merchants.

- Tabby: A Gulf-based BNPL app that has extended its services to Jordan.

- Arab Bank: Introduced a debit-card-based BNPL feature within its Arabi Mobile application.

This segment reflects global trends, offering consumers flexible instalment payments and boosting merchant sales.

Revenue-Based Financing (RBF)

Revenue-linked financing is emerging as an alternative for SMEs:

- Flow48: A regional fintech providing revenue-based SME financing solutions, active in Jordan.

- Liwwa: While primarily an invoice financing platform, its model is adjacent to RBF, enabling SMEs to access working capital tied to receivables.

These approaches align repayment schedules with business performance, offering flexibility for entrepreneurs.

Vehicle Finance

Vehicle-related credit remains an important channel, supported by multiple providers:

- Banks: Offer car loans with long tenors (up to 7 years) and high loan-to-value ratios.

- Leasing companies: Key players include Capital Leasing, Etihad Leasing, and Tamallak, providing asset-backed financing.

- Microfinance institutions (MFIs):

- Microfund for Women (MFW): Provides a Public Vehicle Loan product.

- Tamweelcom: Offers specialised vehicle financing solutions.

This segment plays a critical role in enabling income-generating activities and improving mobility for individuals and small businesses.

Comparative Snapshot of Lending Models in Jordan

For quick reference, the table below summarises the key lending models and their main players in Jordan’s NBFI sector:

Factors Driving Growth

Several dynamics underpin the continued expansion of Jordan’s non-bank financial institutions (NBFIs):

Large Underserved Market

- Around 61% of adults remain unbanked (World Bank Findex, 2021).

- This creates substantial room for NBFIs to reach financially excluded populations and provide alternatives to informal lending.

Middle-Class Consumer Needs

- A growing young and middle-class demographic is driving demand for consumer credit to cover electronics, education, healthcare, and emergencies.

- The popularity of Buy Now, Pay Later (BNPL) models reflects this rising preference for instalment-based credit solutions.

Regulatory Support

- The Central Bank of Jordan (CBJ) has prioritised financial inclusion through dedicated strategies.

- Initiatives such as the regulatory sandbox and the introduction of crowdfunding regulations support innovation while maintaining oversight.

Foreign Funding

- Jordan’s NBFIs attract capital from development finance institutions (DFIs) such as the U.S. DFC and FMO.

- Investment platforms like Esketit and Bondster channel global retail funds into Jordan’s consumer loan originators.

Technology and Innovation

- Use of AI-based credit scoring, mobile wallet integration, and app-based loan applications has improved efficiency, broadened outreach, and reduced friction in customer onboarding.

Challenges Impacting NBFIs

Despite strong growth opportunities, non-bank financial institutions (NBFIs) in Jordan face several structural and market challenges that affect both profitability and long-term sustainability.

Credit Risk:

Many NBFIs serve higher-risk client segments, which makes their portfolios more vulnerable to defaults.

Rising portfolio-at-risk (PAR) ratios have placed additional pressure on asset quality, highlighting the need for robust credit assessment and recovery mechanisms.

Operating Costs:

Although digital channels are expanding, a branch-heavy model remains necessary to meet regulatory know-your-customer (KYC) requirements and to build customer trust.

This physical presence significantly raises cost-to-serve, particularly in dispersed rural areas where outreach is resource-intensive.

Competition:

The NBFI market is becoming increasingly crowded.

More players in the same customer pools heighten the risk of borrower over-indebtedness while simultaneously exerting downward pressure on interest margins.

Compliance:

Adhering to the Central Bank of Jordan’s stricter licensing, governance, and reporting standards requires substantial investment in technology systems, organisational upgrades, and stronger capital adequacy.

These obligations add to the operational burden for smaller or emerging institutions.

Macroeconomic Risks:

Jordan’s macroeconomic environment compounds the challenges for NBFIs.

The dinar’s peg to the U.S. dollar means that U.S. interest rate hikes feed directly into domestic funding costs.

Additionally, regional instability can threaten liquidity flows and limit the availability of affordable funding.

Sector Stability and Outlook

Despite multiple challenges, Jordan’s NBFI sector remains stable, resilient, and vital for advancing financial inclusion.

Both microfinance institutions (MFIs) and fintech lenders are continuing to expand their outreach.

Reforms by the Central Bank of Jordan (CBJ) have successfully integrated informal lenders into the regulated system, enhancing transparency and credibility.

Looking ahead, consolidation among players is possible. However, strategic partnerships such as MFIs collaborating with e-wallet providers are already reshaping the ecosystem.

NBFIs are expected to remain central to MSME and consumer finance as Jordan pursues more inclusive economic growth.

Fintech, Digital Lenders, and Innovation

High smartphone penetration of around 85% has supported the rapid growth of fintech-driven lending.

- Money for Finance (MFF) and Lendo combine digital onboarding with a physical branch presence, balancing speed, convenience, and trust.

- Loyalty programmes and instant approvals drive retention rates above 90%, highlighting customer stickiness.

- Liwwa pioneered SME crowdfunding, using automated credit scoring and attracting institutional investors to expand its funding base.

- Traditional MFIs are also embracing digital transformation, digitising operations, piloting mobile apps, and leveraging partnerships with mobile wallets such as Zain Cash and Dinarak.

- The CBJ has actively supported innovation by introducing electronic KYC (eKYC), upgrading the credit bureau, and maintaining a regulatory sandbox for fintech pilots.

Peer-to-Peer Lending and Crowdfunding

Jordan’s peer-to-peer (P2P) lending and crowdfunding market is still nascent but highly promising.

- Liwwa was the first mover, but new crowdfunding regulations introduced in 2024 have now created a legal framework for licensed platforms.

- This allows diaspora investors and retail investors to channel funds via platforms such as Esketit and Bondster, linking foreign capital with local borrowers.

- The CBJ enforces prudential limits to safeguard investors and consumers.

- Sandbox pilots are experimenting with niche use cases, including refugee financing and student loans.

- The first wave of fully licensed platforms is expected to emerge by 2025–2026.

Conclusion

Jordan’s economy, while facing structural challenges, is being strengthened by the growth of its NBFI sector.

From microfinance institutions to fintech-driven models such as BNPL, RBF, and vehicle loans, these organisations are expanding financial access, supporting SMEs, and deepening financial inclusion.

Regulatory reforms spearheaded by the CBJ have provided a solid foundation for growth and resilience.

Going forward, NBFIs will remain at the heart of Jordan’s financial inclusion targets, playing a decisive role in sustaining economic stability and resilience across the country.

Sources

- World Bank. Jordan: Growth and Competitiveness Development Policy Financing – Program Document. Washington, DC: World Bank, 2025.

- Esketit. “How Money for Finance Took Over Jordan.” Esketit Blog, 2025.

- Esketit. “Jordan’s Money For Finance Shows Excellent Results.” Esketit Blog, 2021.

- Bondster. “Lendo is a New Provider on Bondster.” Bondster News, 2022.

- Tanmeyah. Microfinance Sector Performance Report – Q4 2023. Amman: Tanmeyah, 2025.

- Chris Statham. The Jordan DFS Landscape – A Situation Analysis. Digital Frontiers Institute, 2019.

- The Jordan Times. “Jordan Post and Money for Finance to Expand Services.” The Jordan Times, 2022.

- FMO. “Project Detail – Liwwa Inc.” FMO.nl, 2021.

- Wamda. “Jordan’s liwwa Secures $5 Million Loan from DFC.” Wamda.com, 2021.

- IMF. Jordan: 2024 Article IV Consultation – Staff Report. Washington, DC: IMF, 2024.

- World Bank. Global Findex Database 2021: Jordan. Washington, DC: World Bank, 2022.

- Heritage Foundation. “Index of Economic Freedom 2025 – Jordan Profile.” Heritage.org, 2025.

Disclaimer Notice

This page is provided for general informational purposes only and does not constitute legal, financial, or investment advice. Please refer to our Full Disclaimer for important details regarding eligibility, risks, and the limited scope of our services.

Disclaimer Notice

This page is provided for general informational purposes only and does not constitute legal, financial, or investment advice. Please refer to our Full Disclaimer for important details regarding eligibility, risks, and the limited scope of our services.

![Non-Bank Financial Institutions and Private Credit Investment in Uzbekistan [2026 Update]](https://cdn.prod.website-files.com/625628af6992eb6ba8dd5c41/67bee8416ef9820506b5e8c8_nbfi-and-private-credit-investment-in-uzbekistan-thumbnail.avif)