Audience Context: The Cash-Rich, Yield-Poor Tech Veteran

High-net-worth individuals (HNWIs) emerging from tech success — ex-FAANG engineers, startup founders, and unicorn alumni often find themselves “cash-rich, yield-poor.”

After liquidity events such as IPOs or acquisitions, they sit on significant cash reserves.

Yet, traditional safe havens are underwhelming:

- Inflation has eroded the value of idle cash.

- Bank deposit rates barely kept up for years.

- Tech-heavy portfolios have been on a rollercoaster (the Nasdaq Composite plunged 33% in 2022 alone).

- Speculative bets like crypto or venture investments have delivered stomach-churning volatility.

Pain Points Faced by Tech HNWIs

- Eroding Cash Value

- Inflation spiked to multi-decade highs, making holding cash costly in real terms.

- Even with recent rate hikes, “safe” deposits often yield less than inflation, shrinking wealth over time.

- Volatile Tech Holdings

- Concentrated positions in tech stocks or startup equity tie fortunes to a highly volatile sector.

- Market downturns can wipe out years of paper gains overnight.

- Limited Yield Options

- Traditional fixed income offered meager returns for much of the past decade.

- Many tech executives earn near-zero on cash or low single digits on bonds—paltry for “yield-poor” millionaires seeking passive income.

- Overexposure & Lack of Diversification

- Wealth built on the tech wave now leaves portfolios overexposed to tech sector risk.

- Relying solely on equities or speculative crypto creates a single point of failure.

The Shift Toward Private Credit

These challenges set the stage for an asset class that addresses all of the above: private credit.

- A form of alternative investment that turns cash-rich tech wealth into steady, attractive income.

- Surveys show HNWIs now allocate roughly 20–30% of their portfolios to alternative assets, with private credit forming a growing share.

- This shift accelerated after repeated market disruptions exposed the limitations of stock-heavy portfolios.

- Seasoned tech entrepreneurs and executives are actively seeking high-yield investments that deliver stability and diversification — rather than chasing the next speculative win.

Why Private Credit Works for Tech HNWIs

Private credit, often in the form of private debt funds, direct lending, or other non-bank loans, has emerged as a compelling solution for cash-rich, yield-hungry investors.

It offers a combination of steady returns, predictable income, and diversification that directly addresses the pain points of tech millionaires.

Key Advantages of Private Credit

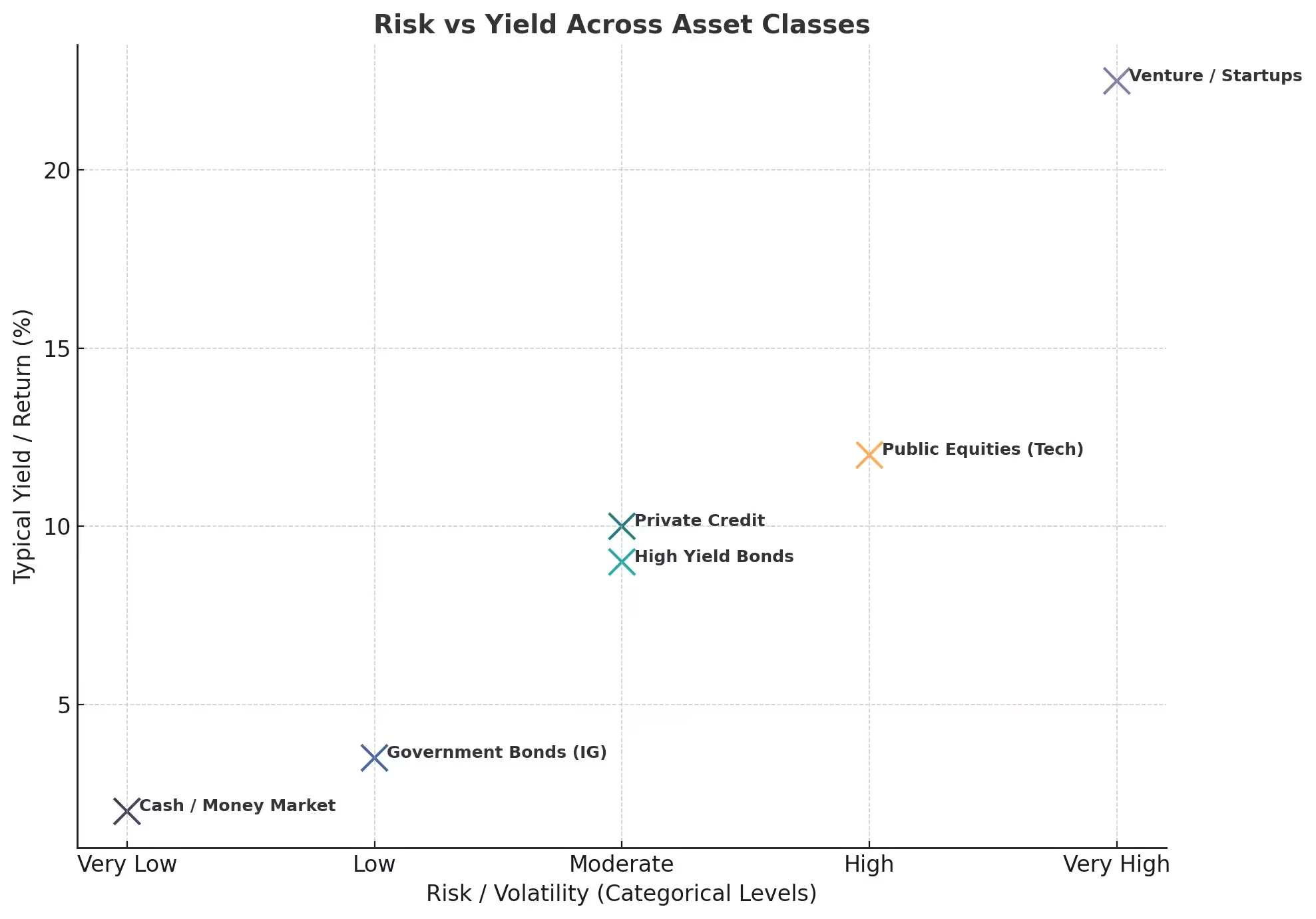

1. Attractive, Stable Returns

- Targets high single-digit to low teens annual returns (8–12%), far surpassing bond yields and bank deposits.

- Returns come primarily from interest payments on loans and have been remarkably consistent.

- Senior direct lending strategies have historically delivered around ~9% annually over the past decade, even outpacing global equities.

- Crucially, returns are contractual and steady, not dependent on speculative equity upside.

2. Passive Income and Cash Flow

- Private credit provides monthly or quarterly cash flow, a major draw for HNWI investors.

- Unlike equities, which may require selling stock or waiting for dividends, loans pay out interest income regularly.

- These predictable payments—often monthly—create a reliable passive income stream that most asset classes can’t match.

- In contrast to the feast-or-famine of tech stock gains, this is passive income on autopilot.

3. Low Correlation and High Diversification

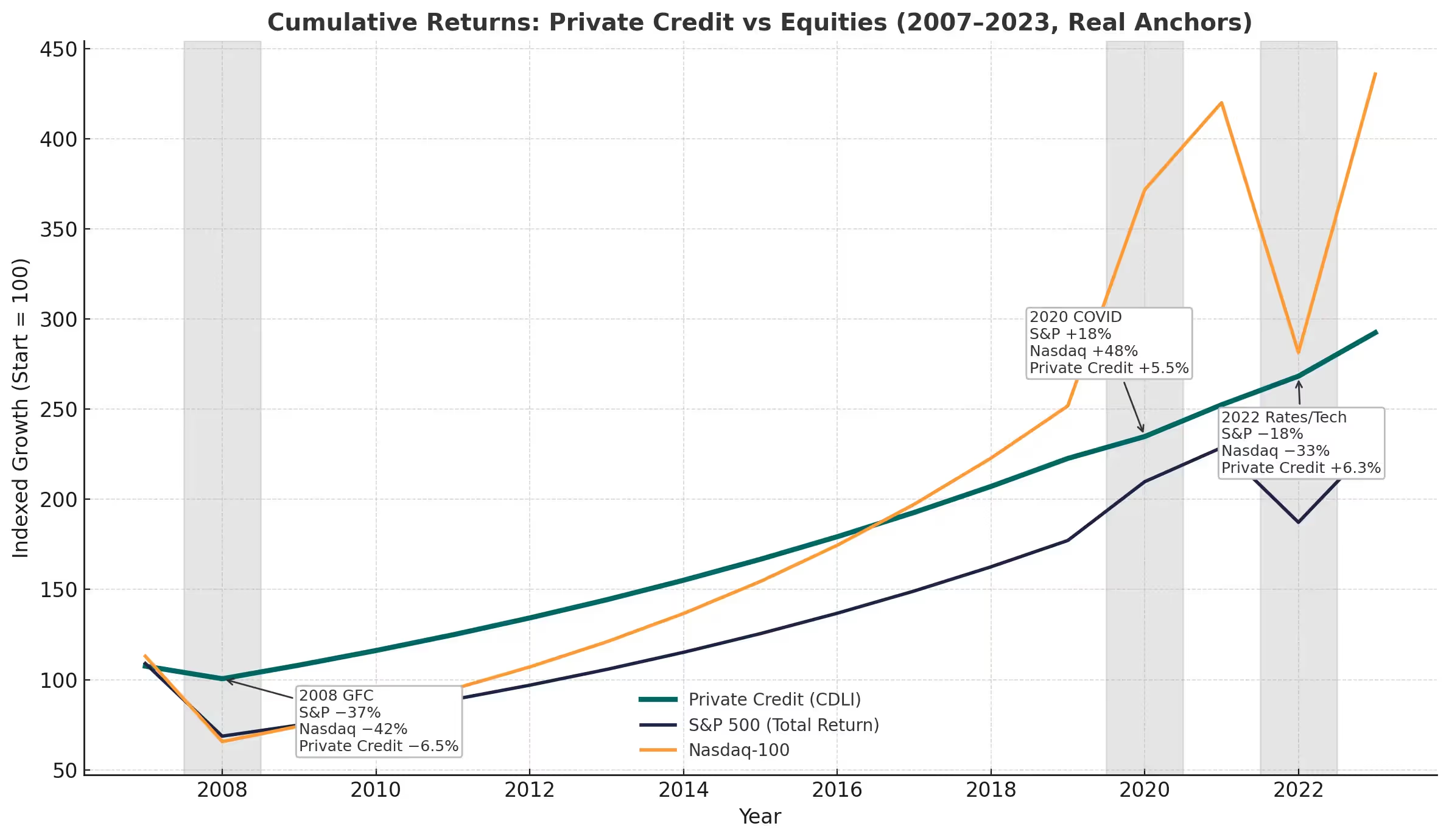

- Private credit returns have a low correlation to public markets.

- Whether the Nasdaq soars or crashes, a portfolio of loans to middle-market companies tends to remain stable.

- This diversification reduces sensitivity to stock market volatility.

- During downturns, well-structured private credit funds often continue paying interest, acting as a stabilizer amid chaos.

4. Tolerable Illiquidity – for Those Who Can Afford It

- Capital must be locked up for a period (often 1 to 5+ years).

- This illiquidity is the trade-off for higher yield — investors can’t exit at will.

- HNW tech investors can typically afford this trade-off and, in return, capture the “illiquidity premium”—often several percentage points above comparable public-market debt.

- Best suited for capital not needed immediately (not for emergency funds).

5. Institutional-Grade Deals, Now Accessible

- Historically, top-tier private credit deals were exclusive to pension funds, banks, and asset managers.

- Today, platforms and funds have democratized access for HNWIs.

- Specialised platforms (some like the “AWS of finance”) pool capital from wealthy individuals into institutional-grade loan deals.

- The investor base has broadened beyond Wall Street to include family offices and accredited individuals.

- Example: a tech millionaire can now allocate $500K–$1M into a private credit fund or BDC and gain diversified exposure once off-limits.

- Fintech innovation is further improving access and transparency, appealing to analytical, data-driven tech investors.

Comparative Performance of Major Asset Classes

Why It Fits Tech HNWIs’ Risk Profile

- It’s not about chasing another 10x homerun.

- Instead, it’s about a solid 8–10% return that reliably shows up every year.

- As one wealth manager quipped: “Traditional bonds today offer return-free risk, while private debt offers risk-adjusted returns.”

- For cash-rich but yield-starved investors, private credit flips the script — putting money to work with meaningful yields without betting the farm on volatility.

{{cta-component}}

Tech-Culture Parallels: Speaking the Engineer’s Language

The world of private credit resonates with many tech professionals’ mindset.

These are individuals who built careers on data-driven decision making, systems thinking, and platform scalability.

Private credit, in many ways, speaks the same language.

Data-Driven, Analytical Approach

- Successful lending is all about rigorous risk assessment — analysing cash flows, balance sheets, collateral, and probabilities of default.

- This appeals directly to the engineer’s brain.

- Tech investors accustomed to A/B testing, KPIs, and metrics appreciate that private credit deals come with detailed data to analyse:

- Financial statements

- Covenants

- Credit ratings

- It’s an analytical, numbers-driven investment process, much like evaluating a SaaS business’s metrics, rather than the hype-fueled guessing game of early-stage startup investing.

Reducing Single Points of Failure

- In engineering, a single point of failure is unacceptable.

- In tech portfolios, holding all wealth in one asset class (e.g., tech equities or one’s own company stock) creates the same risk.

- Private credit provides redundancy:

- If public stocks crash, the private credit allocation can continue performing independently.

- This offers “uptime” for the overall financial plan, much like a fail-safe system keeping operations running during downtime.

- Tech executives intuitively understand the value of such backup systems.

Platform Thinking – Finance as a Service

- The rise of private credit platforms mirrors the rise of cloud infrastructure in tech.

- Just as AWS and cloud platforms revolutionised computing with on-demand scalability, private credit platforms deliver “plug-and-play” access to alternative investments.

- Investors don’t need to build a lending business from scratch. Instead, they:

- Subscribe to platforms or funds handling origination, underwriting, and servicing.

- Outsource complexity while gaining exposure to institutional-grade credit opportunities.

- For tech professionals accustomed to scaling via platforms and APIs, this feels natural.

- Firms like Kilde are positioning themselves as authorities in this space—effectively the “AWS of finance.”

Risk Mitigation = Bug Testing

- Engineers and product managers spend hours testing for edge cases and anticipating failures.

- Private credit employs similar thinking:

- Covenants and collateral act as “code” anticipating what could go wrong.

- Example: a covenant might trigger intervention if a borrower’s revenue drops too sharply — like a system alert in software.

- These structured protections offer a sense of control, contrasting with the wild volatility of equity markets.

Cultural Alignment with Tech Investors

Private credit offers a pragmatic, design-driven approach to investing. It mirrors how tech professionals approach problems:

- Resilient systems → diversified portfolios.

- Scalable design → platforms handling complexity.

- Efficient processes → predictable cash flows and data-driven decisions.

Investing through private credit platforms or funds can feel like using a sophisticated tool — abstracting away complexity while maintaining transparency with dashboards and data.

This cultural alignment makes the leap into private credit even more natural for a tech-savvy audience.

Smarter Portfolio & Legacy Planning with Private Credit

For many tech HNWIs, the goal has shifted from aggressive wealth creation to wealth preservation and steady growth.

After years of concentrating wealth in high-growth tech assets, they now seek a more balanced, resilient portfolio for the long run.

Private credit is increasingly playing a key role in this “smart diversification” and legacy planning.”

1. Diversification Away from Tech Concentration

Former tech executives often have their net worth tied up in FAANG shares or their own exited company’s stock.

This creates portfolios overly correlated with the tech sector or even a single company.

Allocating a portion into private credit helps hedge against tech downturns.

With its low correlation to equities, private credit tends to remain stable even if the Nasdaq or S&P 500 stumble.

2. Passive Income for Life and Legacy

Private credit investments often provide monthly income, valuable for lifestyle planning and legacy goals.

Wealthy tech families use steady cash flow to:

- Fund living expenses.

- Support philanthropic endeavors.

- Build family trusts.

Example: A 9% annual yield on multimillion-dollar allocations can generate six-figure passive income, without touching principal.

Crucially, this strategy preserves principal for heirs or charities.

In wealth transfer planning, sustainable income > speculative growth that may or may not materialise.

Private credit acts as the “golden goose” consistently laying eggs (interest income) for both current needs and future generations.

3. Countering “Tech-Beta” with Stability

Many tech HNWIs are over-indexed to the tech industry (“tech-beta”).

Assets like tech stocks, funds, startup equity, and even crypto often move together under macro pressures (rising rates, geopolitics, inflation).

Private credit provides exposure to the real economy, often insulated from tech swings.

Borrowers may include:

- Mid-sized manufacturers

- Healthcare companies

- Real estate projects

- Other non-tech enterprises

This means wealth is not dependent on a single sector.

In uncertain macro environments, private loans act as a stabiliser.

Notably, many private credit strategies use floating interest rates — so when rates climb, income adjusts upward, hedging against inflation and rate changes.

4. Multi-Generational Wealth Strategy

After major liquidity events, tech entrepreneurs naturally start thinking about legacy.

Private credit is increasingly used as a tool for intergenerational wealth transfer, because of its stability.

Unlike speculative investments that may boom or bust, private credit can deliver consistent income across market cycles.

Family offices favor private credit since it:

- Preserves capital.

- Provides predictable income.

- Fits easily into trusts or family funds designed to last decades.

Its expected outcomes — steady income, low volatility—align with ultra-long-term wealth goals.

5. The Big Picture: A Second Act for Tech Wealth

Portfolio diversification here is not a buzzword; it’s a safety mechanism.

Adding private credit to a Nasdaq-heavy portfolio is like adding ballast to a ship, keeping it stable in rough seas.

For legacy planning, it offers a way to engineer a financial engine that powers family wealth for generations.

Increasingly, tech HNWIs recognise that after the high-growth phase, the prudent “second act” is about:

- Wealth preservation

- Passive income generation

Private credit is emerging as the ideal second act for sustaining tech fortunes.

{{cta-component}}

Myths & Misconceptions about Private Credit

Despite its merits, private credit as an asset class is often misunderstood.

Below are three common myths tech investors may encounter — alongside the reality.

Myth #1: “Private Credit is basically Private Equity, just another high-risk alternative.”

Reality:

Both fall under private market investments, but they are fundamentally different.

- Private credit = lending money (debt).

- Private equity = owning a stake in a company (equity).

Key Differences

- Return Profile:

- Private credit: predictable, steady returns from set interest payments.

- Private equity: returns rely on company growth or a future sale.

- Risk:

- Private equity may deliver higher upside if a company rockets, but also carries higher risk of losses (equity holders are last in line in bankruptcy).

- Private credit investors are higher in the capital stack—often with collateral—and don’t depend on exits.

- Portfolio Role:

- Private credit: generally lower risk, lower volatility, focused on income.

- Private equity: higher risk, focused on capital appreciation.

In short, private credit is closer to fixed income with an illiquidity twist than to venture capital.

Savvy investors often hold both — using private credit for stability and portfolio diversification, and private equity for potential high growth.

Myth #2: “Private Credit is too risky – isn’t lending to private companies like throwing money into a black box?”

Reality:

- Yes, private credit involves lending to non-public entities that may lack formal credit ratings, so there is credit risk.

- However, the track record in senior secured lending has shown low default and loss rates in well-managed funds.

Evidence of Resilience

- Data shows lower volatility and limited downside compared with equities.

- During crises (e.g., the 2020 pandemic), many private credit funds continued timely payments while public markets seesawed.

- Structural protections — collateral and covenants — act as safeguards.

- One study noted that in COVID-19 downturns, private credit losses were about half those of high-yield public bonds, illustrating resilience.

Strategy Options

- Riskier strategies exist (e.g., mezzanine loans, distressed debt).

- But HNW investors can choose conservative strategies:

- Senior loans

- First-lien security

- Strong covenants

With proper due diligence and experienced managers, private credit is not a blind gamble.

Instead, it’s a high-yield investment with carefully managed risk.

Myth #3: “Private Credit is illiquid and exclusive – you need tens of millions and must lock money away forever.”

Reality:

Yes, private credit is less liquid than stocks — capital is typically locked up for a few years.

However, it’s not a lifetime lock-up, and many funds now offer quarterly or periodic liquidity windows.

Accessibility Today

- The idea that only mega-institutions can access private credit is outdated.

- Today, accredited investors can participate starting in the low six figures through:

- Feeder funds

- Private credit funds

- Fintech platforms

- The rise of non-traded BDCs and online platforms has broadened access.

- Family offices and HNW individuals are among the fastest-growing groups allocating to private credit.

Improving Liquidity Options

New fund structures and even the prospect of private credit ETFs are improving access.

Investors who don’t need immediate liquidity can comfortably allocate a portion of capital to private credit to earn the illiquidity premium.

In Summary

Private credit is not a mysterious or ultra-risky niche reserved for banks. It’s a diverse asset class, ranging from conservative to opportunistic strategies.

As more data and success stories emerge, misconceptions are fading.

For tech investors accustomed to debugging code and analyzing systems, private credit can become the stable workhorse in a portfolio — not an unstable bet.

{{cta-component}}

Future Outlook: Private Credit as Tech Wealth’s “Second Act”

The convergence of tech wealth and private credit is only beginning.

Looking ahead, several trends suggest that private credit will become an even more integral part of how HNWIs, especially those from tech backgrounds, manage and diversify their wealth.

1. Continued Growth and Mainstreaming

The private credit market is experiencing explosive growth.

Globally, it’s forecast to exceed $3.5 trillion in assets by 2028, as more investors pile in and borrowers seek alternatives to bank loans.

As the market scales, expect:

- More products tailored for individuals.

- More secondary market options (e.g., trading private loan interests).

- More integration with wealth management platforms.

Much like private equity a decade ago, private credit is moving from the periphery to mainstream acceptance.

For tech executives — often early adopters — getting in now positions them ahead of the curve of this financial evolution.

2. Behavioral Shift: From Growth Chasing to Yield Harvesting

During wealth creation, tech entrepreneurs focused on high growth, embracing risk and volatility.

In wealth preservation, the mindset shifts:

- Engineers enjoy private credit’s predictable, system-like structure—something to optimise rather than gamble on.

- Executives see it as a strategic allocation for steady execution, similar to running a mature business versus a startup.

This evolution means more tech millionaires will embrace the role of lender.

It’s almost poetic: after years of borrowing VC money and bank loans, they now become the financiers, enjoying steady interest on the other side of the table.

3. Technology’s Influence on Private Credit

Technology is making private credit more appealing:

- AI and big data enhance credit risk models and due diligence, reducing risk and boosting transparency.

- Blockchain and smart contracts may streamline servicing and settlement.

The fintech revolution tech investors once built is now looping back to improve their investments.

In the near future, monitoring a private credit portfolio could be as easy and data-rich as tracking stocks: dashboards showing loan exposures, risk factors, and cash flows.

This will erase much of the historical information asymmetry in alternatives—a major win for analytical investors.

4. Macro Environment Favors Private Credit

Global forces like interest rates, inflation, and geopolitics make private credit increasingly attractive.

Banks are pulling back on lending, creating space for private lenders.

In a “higher for longer” rate environment, private credit benefits from:

- Floating rates

- Higher spreads

In uncertain times, private credit’s diversification benefits make it a portfolio stabiliser.

The next generation of tech wealth—crypto founders, Web3 entrepreneurs—may be even more open to alternatives.

Private credit could serve as the bridge between volatile new wealth and stable old-school finance — a new safe asset for those sceptical of bonds.

5. Private Credit as the New “Second Act”

Successful tech figures often transition from building wealth to preserving and deploying it strategically.

Private credit fits this narrative as the “second act.”

After the thrill of creating a fortune in tech, investors can:

- Deploy that fortune into private credit.

- Generate passive income and support impactful projects.

It offers a sense of continuing to build—funding companies and bridging financing gaps—but with lower risk.

Psychologically rewarding: still part of innovation and growth, but from the driver’s seat of the lender, not the operator.

For many, it’s the ideal blend: staying engaged without the 80-hour startup grind.

In Summary

The future looks bright for the marriage of tech wealth and private credit.

From Silicon Valley to Bangalore, HNWIs are likely to make private credit a portfolio staple in the next decade.

- It aligns with evolving goals of stability and preservation.

- It leverages the very innovations tech leaders pioneered — platforms, data, analytics — to make an old concept (lending) new again.

- As accessibility improves, the narrative will shift from “Why private credit?” to “Which private credit strategy is right for you?”

A clear sign of a maturing trend.

Key Takeaways for the Tech HNWI Investor

Private credit offers a pragmatic and strategic solution for high-net-worth tech investors who are transitioning from aggressive wealth creation to long-term stability and legacy planning.

1. Your Cash Needs to Work Harder

Sitting on large cash holdings is a losing strategy in the long run.

Inflation steadily erodes idle cash, while traditional bonds may not cover the gap.

Private credit allows cash to work, generating high single-digit yields that outpace inflation and provide passive income.

Bottom line: Cash is no longer king – cash flow is.

2. Diversify Your Tech-Heavy Portfolio

Years of success in the tech sector often leave portfolios overexposed to the same risk factors.

Private credit acts as a powerful diversifier, thanks to its low correlation with equities (especially tech stocks).

It serves as a stabilizer, reducing overall volatility.

Analogy: It’s like adding a different engine to your financial vehicle — one that keeps running when the other sputters.

3. Stable Yield, Lower Volatility = Peace of Mind

- Private credit sits in an attractive risk/reward sweet spot:

- 8–10% annual returns, consistently achievable.

- Relatively low volatility.

- Robust downside protections.

- This means:

- Steady passive income, often paid monthly.

- Fewer sleepless nights watching stock tickers.

- For those prioritizing passive income and preservation, it’s hard to ignore.

4. Platforms Democratize Alternative Investing

Fintech innovation has made accessing alternative assets easier than ever.

Dedicated private credit platforms and funds — including firms like Kilde — provide seamless ways to invest in diversified loan portfolios once reserved for banks and institutions.

The landscape has shifted from exclusive club to open marketplace, empowering HNWIs to:

- Deploy capital effectively.

- Diversify wealth without a large in-house analyst team.

In essence, the tools to diversify into private credit are now at your fingertips.

5. Think Long-Term & Legacy

Private credit is not about quick flips, but about building a long-term income engine.

Allocating part of wealth to private credit creates a stable financial foundation to:

- Support lifestyle needs.

- Fund new ventures or philanthropy.

- Extend wealth into future generations.

Many tech leaders are future-proofing fortunes this way—turning volatile equity gains into a steady, enduring legacy.

Closing Thought

For the “cash-rich, yield-poor” tech elite, private credit provides the path to becoming “cash-rich, yield-smart.”

It is a strategy to:

- Preserve and grow wealth intelligently.

- Leverage stability and income in a world that often rewards only high-risk moves.

- Ensure wealth not only survives but thrives for decades — while working as hard as its owners once did.

{{cta-component}}

References:

- Bloomberg. “NASDAQ Composite Index.” Last modified December 31, 2022. https://www.bloomberg.com/quote/CCMP:IND.

- Capgemini Research Institute. World Wealth Report 2025: Digital Strategies for Next-Gen High-Net-Worth Investors. Paris: Capgemini, June 2025. https://www.capgemini.com/insights/research-library/world-wealth-report-2025/.

- Capgemini Research Institute. World Wealth Report 2024: Wealth Management Insights for High-Net-Worth Individuals. Paris: Capgemini, June 2024. https://www.capgemini.com/insights/research-library/world-wealth-report-2024/.

- Cliffwater LLC. Cliffwater Direct Lending Index: Fact Sheet. Los Angeles: Cliffwater, 2024. https://www.cliffwaterdirectlendingindex.com.

- Deutsche Bank Research. Private Credit: A Rising Asset Class Explained. Frankfurt: Deutsche Bank, 2023. https://flow.db.com/trust-and-agency-services/private-credit-a-rising-asset-class-explained.

- Hubbis. “Private Credit: The New Frontier in Wealth Management for 2025.” Hubbis, October 2024. https://www.hubbis.com/article/private-credit-the-new-frontier-in-wealth-management-for-2025.

- Hubbis. “Unpacking Private Credit: Radek Jezbera Explores Its Resilience and Returns at the Hubbis Investment Forum.” Hubbis, October 14, 2024. https://www.hubbis.com/article/unpacking-private-credit-radek-jezbera-explores-its-resilience-and-returns-at-the-hubbis-investment-forum.

- Investopedia. “Private Credit vs. Private Equity: What’s the Difference?” Last modified July 2024. https://www.investopedia.com/private-credit-vs-private-equity-7565530.

- J.P. Morgan Private Bank. “Why Private Credit Remains a Strong Opportunity.” Private Bank Insights, 2023. https://privatebank.jpmorgan.com/nam/en/insights/markets-and-investing/why-private-credit-remains-a-strong-opportunity.

- Moschetti Law Group. “Why High-Net-Worth Investors Choose Debt Funds for Stable Returns.” Moschetti Law Blog, 2022. https://www.moschettilaw.com/why-high-net-worth-investors-choose-debt-funds-for-stable-returns.

- Moschetti Law Group. “Alternative Investments for HNWI: Allocation Trends.” Moschetti Law Blog, 2022. https://www.moschettilaw.com/alternative-investments-hnwi.

- Preqin Ltd. Global Private Debt Report 2023. London: Preqin, 2023. https://www.preqin.com/insights/research/reports/preqin-global-private-debt-report-2023.

- Preqin Ltd. “Global Alternatives AUM on Course to Exceed $30 Trillion by 2030; Private Debt Expected to Rise to $2.6 Trillion by 2029.” Preqin Insights, September 18, 2024. https://www.preqin.com/insights/research/reports.

- SoFi. “Private Credit Market to Surpass $3.5 Trillion by 2028.” SoFi Learn, 2023. https://www.sofi.com/learn/content/private-credit-market-outlook.

- SoFi. “Private Credit vs. Private Equity: What Investors Need to Know.” SoFi Learn, 2023. https://www.sofi.com/learn/content/private-credit-vs-private-equity.

- Wikipedia. “2022 Stock Market Decline.” Last modified December 2022. https://en.wikipedia.org/wiki/2022_stock_market_decline.

- Wikipedia. “Nasdaq Composite.” Last modified December 2022. https://en.wikipedia.org/wiki/Nasdaq_Composite.

Disclaimer Notice

This page is provided for general informational purposes only and does not constitute legal, financial, or investment advice. Please refer to our Full Disclaimer for important details regarding eligibility, risks, and the limited scope of our services.

Disclaimer Notice

This page is provided for general informational purposes only and does not constitute legal, financial, or investment advice. Please refer to our Full Disclaimer for important details regarding eligibility, risks, and the limited scope of our services.

![Non-Bank Financial Institutions and Private Credit Investment in Uzbekistan [2026 Update]](https://cdn.prod.website-files.com/625628af6992eb6ba8dd5c41/67bee8416ef9820506b5e8c8_nbfi-and-private-credit-investment-in-uzbekistan-thumbnail.avif)