Rising prices and market swings in recent years have pushed both new and experienced investors toward low-risk investments — options that preserve capital while still offering a reliable return. Singapore is a natural home for them, thanks to a stable economy, its status as a global financial hub, strong regulation by the Monetary Authority of Singapore (MAS), and AAA credit ratings from all three major rating agencies.

One thing has changed sharply in 2026: interest rates have fallen. Six-month Treasury bills now yield around 1.5% (down from over 3.7% in 2023), the latest Singapore Savings Bond pays a 10-year average of just 2.11%, and the best fixed deposits rarely beat 1.6%. Lower rates make it more important than ever to compare your options and understand exactly what is — and isn't — guaranteed.

This guide covers the safest, lowest-risk investment options in Singapore for 2026: how they work, current returns, minimums, lock-ins, and how your money is protected.

If you also want higher-growth options across the full risk spectrum, see our companion guide to the best investments in Singapore.

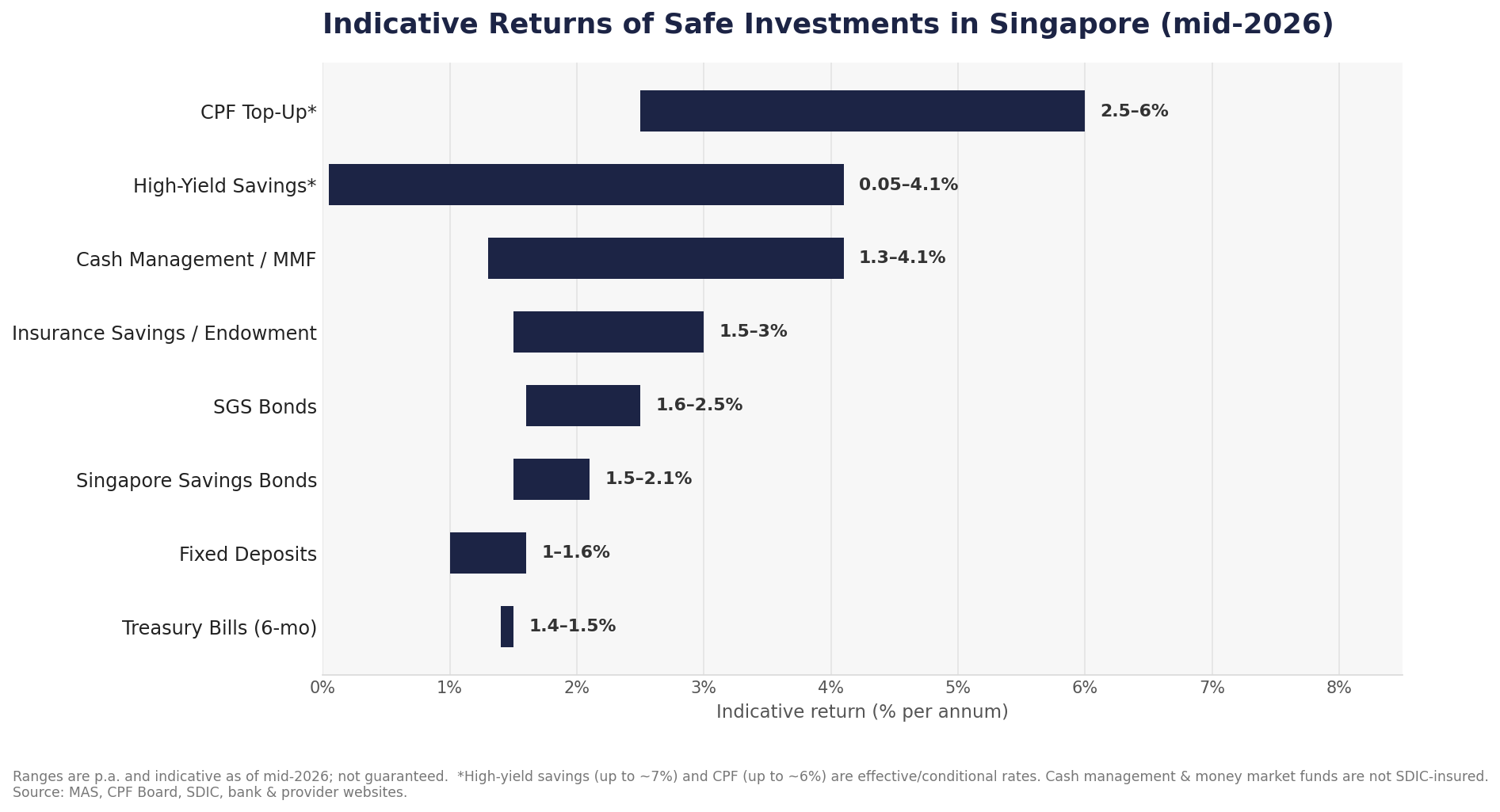

Comparison of the best low-risk investments in Singapore

Here's a quick overview of Singapore's safest investment options and their key features as of mid-2026:

Note: returns are indicative as of mid-2026 and subject to change.

Looking for higher returns and willing to take on more risk? Accredited and institutional investors can also consider Kilde, a MAS-licensed private credit platform with terms of 3 to 36 months. We cover it near the end of this guide — but be clear that private credit is not a low-risk or capital-guaranteed product: it sits well above everything in the table above on the risk scale.

{{cta-component}}

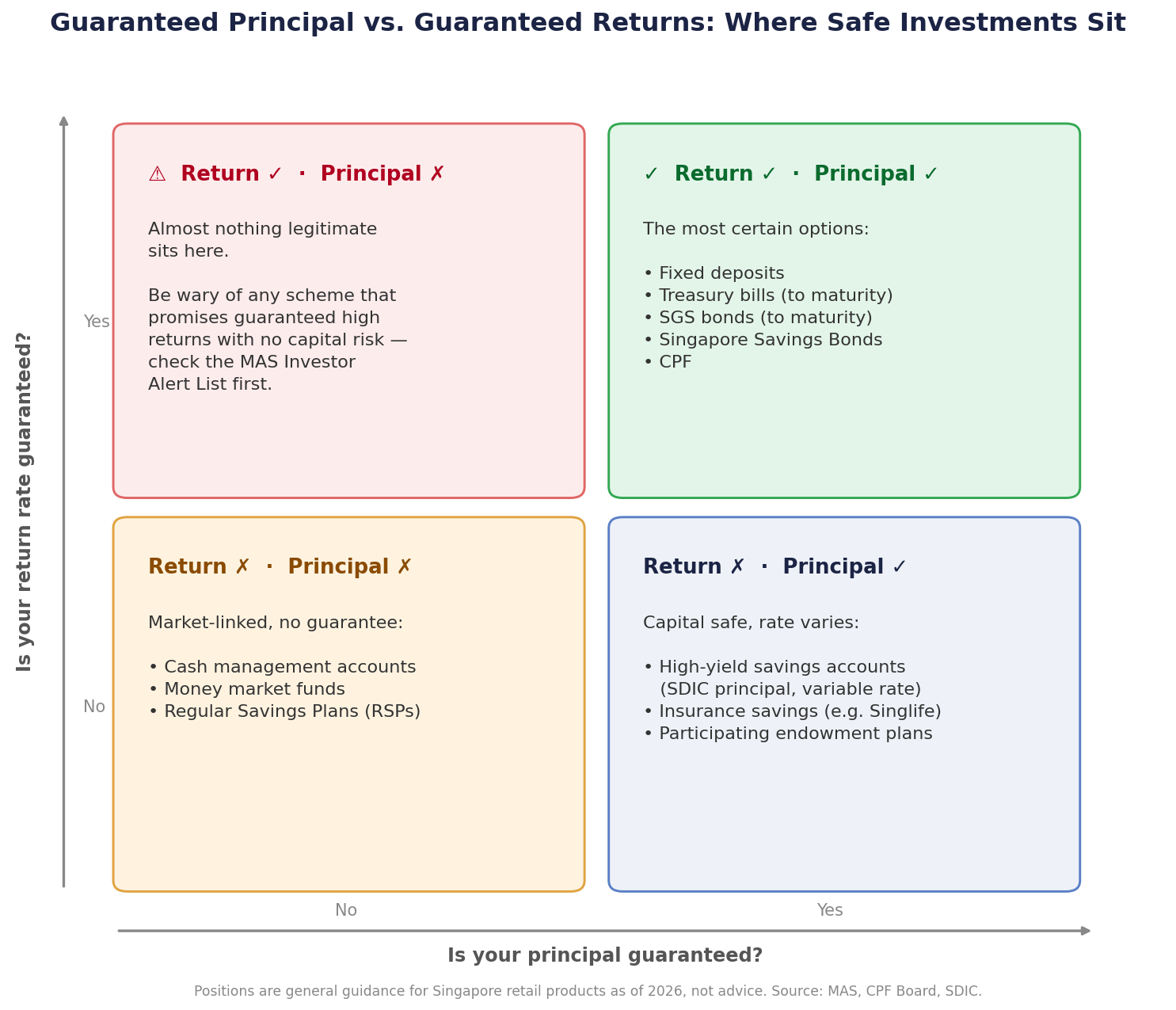

Guaranteed principal vs. guaranteed returns: what "safe" really means

"Safe" and "guaranteed" get used loosely, so it helps to separate two different promises:

- Guaranteed principal (capital-guaranteed): you are certain to get your original capital back. SSBs, SGS bonds and T-bills held to maturity, SDIC-insured deposits, and many endowment/insurance savings plans fall here.

- Guaranteed return: the rate of interest is also fixed and certain. Fixed deposits and SGS coupons qualify; products like the Singlife Account guarantee your capital but not the crediting rate.

Genuinely guaranteed products in Singapore are a short list — government securities, SDIC-insured deposits, CPF, and certain insurance savings plans. If something promises high "guaranteed" returns well above these, treat it with caution and check the MAS Investor Alert List before committing any money.

How safe investments are protected in Singapore

Singapore's low-risk options get their safety from one of three sources.

Singapore Government Securities (SGS)

SGS are debt securities issued and backed by the full faith and credit of the AAA-rated Singapore government — among the safest investments available anywhere. The family includes:

- SGS Bonds (Market Development, Infrastructure and Green SGS).

- Singapore Savings Bonds (SSBs).

- Treasury Bills (T-Bills).

Each serves a different purpose, covered in detail below.

SDIC deposit insurance

The Singapore Deposit Insurance Corporation (SDIC) insures eligible SGD deposits up to S$100,000 in aggregate per depositor, per Scheme member (raised from S$75,000 in April 2024). This covers savings, current and fixed deposit accounts, plus SGD funds under the Supplementary Retirement Scheme (SRS).

All full banks and finance companies are Scheme members, including DBS, OCBC, UOB, Maybank, Citibank, CIMB and others. SDIC does not cover foreign-currency deposits, structured deposits, or investment products such as unit trusts and shares.

Policy Owners' Protection (PPF) Scheme

Insurance savings and endowment plans are not bank deposits, but life policies issued by licensed insurers are protected under the Policy Owners' Protection Scheme, also administered by SDIC, subject to scheme limits.

Singapore Government Securities (SGS) Bonds

SGS bonds are the medium- to long-term members of the SGS family, with tenures from 2 to 50 years. They pay a fixed semi-annual coupon, and individuals pay no tax on the interest. You can't redeem them early with the government, but you can sell them on the secondary market (where the price may be above or below what you paid).

The three types of SGS bonds

- Market Development SGS — traditional bonds that support Singapore's debt market, paying fixed semi-annual coupons over 2 to 50 years.

- Infrastructure SGS (SINGA bonds) — finance major long-term infrastructure such as rail lines and coastal protection; they work like Market Development SGS.

- Green SGS — launched in 2022 to fund environmentally sustainable infrastructure; otherwise identical to Infrastructure SGS.

Expected returns and risks

As of mid-2026, SGS bond yields run roughly 1.6% to 2.5% a year depending on tenor — for example, the 2-year SGS bond auctioned in May 2026 cleared at 1.60%, while the 10-year government bond yield was around 2.06% in June 2026. Longer tenors generally pay a little more. While returns are modest, the principal is guaranteed if you hold to maturity. Two risks to keep in mind:

- Interest rate risk: if rates rise after you buy, the bond's secondary-market price falls (newer bonds pay more, making yours less attractive).

- Inflation risk: if inflation outpaces your coupon, your money loses purchasing power over time.

How to invest and minimums

You can buy SGS bonds at primary auctions through DBS, OCBC or UOB (using cash, SRS or CPFIS funds), via brokers on the secondary market, or through SGX-listed bond ETFs. The minimum is S$1,000, in multiples of S$1,000. Check the issuance calendar for upcoming auctions.

Singapore Savings Bonds (SSBs)

Singapore Savings Bonds combine government-backed safety with rare flexibility — unlike SGS bonds, you can redeem in any month, penalty-free, and get your capital plus accrued interest back.

Features and benefits

- Government-guaranteed: fully backed by the Singapore government, the same security as other SGS.

- Flexible horizon: a 10-year maturity, but redeemable any month with no penalty, with proceeds paid by the 2nd business day of the following month.

- Step-up interest: the rate rises the longer you hold, rewarding patience.

- Capital-guaranteed: you always get your principal back — there is no scenario where you lose capital.

- Low entry: start from just S$500 (up to S$200,000 per person), even more accessible than SGS bonds.

- Open to foreigners: any individual aged 18+ with a bank account and CDP account can apply, including non-residents.

Current interest rates

MAS sets each tranche's rates before it opens. The June 2026 issue (SBJUN26) pays 1.46% in year one, stepping up to 2.87% in year ten, for a 10-year average return of 2.11%. SSB rates peaked above 3.3% in 2023–2024 and have since fallen with the broader rate cycle, so today's tranches lock in noticeably less than a couple of years ago.

{{cta-component}}

Treasury Bills (T-Bills)

Treasury bills are the short-term member of the SGS family — among the most popular low-risk investments in Singapore.

How they work

T-bills come in 6-month and 1-year tenors and pay no coupon. Instead, you buy at a discount to face value and receive the full face value at maturity — the difference is your return. For example, buying a S$1,000 T-bill for S$985 gives you S$15 at maturity. The minimum is S$1,000, bought at uniform-price auctions with competitive or non-competitive bids.

Current yields

Yields are set at each auction (the "cut-off yield"). They have fallen sharply: the 6-month T-bill cleared at 1.48% on 4 June 2026 and 1.47% on 18 June 2026, versus 3.6%–4% in 2023–2024. At these levels, T-bills are broadly in line with the best fixed deposits and the latest SSB. They're best for cash you can lock away for the full tenor, since selling early on the secondary market can mean a small loss.

Fixed Deposits (FDs)

Fixed deposits offer a guaranteed return over a set term, typically above a regular savings account, with SDIC protection up to S$100,000. They're simple and predictable — ideal for conservative savers — but you forfeit interest if you withdraw early.

Best FD rates in Singapore (June 2026)

Fixed deposit rates have fallen alongside government yields: the big local banks now offer roughly 1.0–1.25%, while the highest promotions from digital banks and finance companies reach about 1.60% p.a. Foreign-currency FDs (e.g. USD) can pay more but carry currency risk. Rates are as of June 2026 and change frequently — always verify with the bank before placing funds.

What to compare

When choosing the best guaranteed-return fixed deposit, look at the minimum deposit, whether fresh funds are required, the tenure, interest-payment frequency, early-withdrawal penalties, and auto-renewal terms.

{{cta-component}}

High-Yield Savings Accounts

Competition between banks has turned high-yield savings accounts into a flexible, low-risk way to earn more on everyday cash. They pay tiered bonus interest when you meet conditions such as crediting your salary, spending on a card, or investing.

Top accounts (mid-2026)

- UOB One: effective rates up to ~3.4% p.a. on qualifying balances.

- OCBC 360: tiered bonus interest, with effective rates up to roughly 2.45–4.65% p.a. depending on conditions met.

- DBS Multiplier: tiered rates up to ~4.1% p.a. based on income and transactions.

- Standard Chartered Bonus$aver advertises higher headline rates (up to ~7% p.a.) but only when several stringent conditions are met.

Two important caveats. First, banks cut many of these bonus rates through 2025–2026, so headline figures from older guides are often out of date — check the latest before switching. Second, the top rate usually applies only to a capped balance (often the first S$75,000–S$100,000) and requires you to clear multiple hoops each month.

Cash Management & Money Market Funds

Cash management accounts and money market funds park idle cash in short-term instruments such as T-bills, high-quality short-term bonds and bank deposits. They offer no lock-in, low minimums and next-day liquidity — handy as a flexible alternative to a savings account.

As of mid-2026, indicative yields include the Fullerton SGD Cash Fund at roughly 1.3% (7-day annualised), Syfe Cash+ Guaranteed at about 1.2–3.45% across 1–12 month terms, and StashAway Simple Plus at around a 4.1% projected yield-to-maturity. Digital-bank savings options such as MariBank and GXS have also offered competitive rates.

One key distinction for a "safe" portfolio: most cash management portfolios and money market funds are not capital-guaranteed and not SDIC-insured (the "guaranteed" variants that invest into bank fixed deposits are an exception, subject to underlying bank risk). Compare yields, fees and the safety mechanism carefully before choosing.

Insurance Savings & Endowment Plans

Insurance savings plans combine a savings component with life protection. They suit savers who want a guaranteed-return element plus an insurance payout, and the underlying funds are typically invested in low-risk bonds and fixed income.

How they work

You pay regular or single premiums; part covers life insurance and the rest is invested. Many plans are capital-guaranteed — you get 100% of your capital at maturity plus returns via guaranteed interest and (often non-guaranteed) bonuses.

The Singlife Account is a popular example. Its base return is 1.5% p.a. on the first S$10,000 and 1.0% on balances above that up to S$100,000, with effective rates up to roughly 3.5% p.a. through bonus campaigns. It has no lock-in, includes life cover of up to 105% of the account value, and is capital-guaranteed — though, like most such plans, the crediting rate itself is not guaranteed.

Types of plans

Endowment plans

These mature after a set term (commonly 2 to 25 years) and pay a lump sum at maturity. Some endowment plans guarantee returns; others depend partly on the insurer's participating fund. Short-term endowments are a common alternative to fixed deposits — for example, DBS SavvyEndowment tranches have offered around 1.4–1.6% over a 2-year term — though tranches sell out and early exit can mean a loss.

Whole life plans

These provide life insurance coverage plus a cash value that builds over time.

Benefits to weigh

- Capital guarantee on many (not all) plans at maturity.

- Potential bonuses on top of guaranteed returns, based on the participating fund.

- Insurance protection for your beneficiaries alongside savings.

- Possible tax benefits under certain conditions.

- Watch the lock-in: early surrender can cost a significant chunk of your returns or capital.

{{cta-component}}

CPF Top-Ups

The Central Provident Fund (CPF) is Singapore's retirement savings system for citizens and PRs, and topping it up is one of the safest ways to earn a government-backed return.

- Guaranteed interest: 2.5% p.a. on the Ordinary Account (OA) and 4% p.a. on the Special, MediSave and Retirement Accounts (the 4% floor is extended to 31 December 2026). An extra 1% applies to the first S$60,000 of combined balances (capped at S$20,000 for OA), plus a further 1% on the first S$30,000 from age 55 — pushing the effective rate up to about 6% p.a.

- SA closure at 55: since January 2025, the Special Account is closed when a member turns 55; those savings move to the Retirement Account (up to the Full Retirement Sum) or the Ordinary Account.

- Tax relief: cash top-ups qualify for up to S$8,000 of tax relief for yourself and another S$8,000 for family members (S$16,000 total) each year.

- Matched Retirement Savings Scheme (MRSS): the government matches cash top-ups to the RA of eligible members below the Basic Retirement Sum — up to S$2,000 a year with a S$20,000 lifetime cap, with the age cap removed from 2025 (the matched portion does not attract tax relief).

The trade-off: CPF savings are locked for retirement, with withdrawals restricted until the eligible age.

Regular Savings Plans (RSPs)

Regular Savings Plans let you invest a small, fixed amount each month into unit trusts or ETFs. They're a gentle on-ramp to investing:

- Dollar-cost averaging smooths out your entry price and reduces the impact of volatility.

- Low minimums make them accessible — you can start from around S$100 a month.

- Diversification across a basket of holdings.

Note that RSPs invest in market-linked products, so they are not capital-guaranteed and carry more risk than the government-backed options above — they sit at the higher-risk edge of a "low-risk" toolkit.

Beyond low-risk: a higher-yield option for accredited investors

If you've covered your safe, capital-preservation base and are an accredited investor who can take on more risk for more return, private credit is worth understanding. Kilde is a MAS-licensed platform that lets accredited and institutional investors put money into asset-backed private debt issued by non-bank financial institutions in the consumer and SME space — an asset class normally reserved for institutions.

Since launching in 2021, Kilde has delivered an average net return of around 12.39% over the last 12 months (12.6% annualised since inception, 10%+ every year), with a 0.0% default rate to date, fees capped at 0.5%, monthly coupons, and terms of 3 to 36 months.

How it compares to the safe options above:

- Higher target returns: where SSBs and T-bills now yield roughly 1.5–2.1%, Kilde targets up to ~15% p.a.

- Shorter than insurance plans: 3–36 month terms, versus the 5–25 years typical of endowments.

- Collateral and diligence: deals are secured by collateral and screened through credit analysis — which mitigates, but does not remove, risk.

- Lower correlation to public market swings.

Important: private credit is not a low-risk or capital-guaranteed investment. Unlike SSBs, T-bills, SDIC-insured deposits or CPF, your capital is genuinely at risk, and the investment is open only to accredited and institutional investors. It belongs in the growth, not the capital-preservation, part of a portfolio.

{{cta-component}}

How to build your low-risk investment strategy

Match your choices to your goals, risk tolerance and time horizon:

- Short-term (cash you may need soon): T-bills, fixed deposits, the redeemable SSB, high-yield savings or cash management accounts.

- Medium-term: SSBs and short-term endowment plans.

- Long-term retirement: CPF top-ups and longer endowment plans.

A few principles for low-risk investing:

- Know what's guaranteed. Prioritise government-backed securities, SDIC-insured deposits and CPF for true capital preservation.

- Diversify across instruments so no single product or institution dominates your safe allocation.

- Keep liquidity for emergencies — hold some cash in flexible, no-penalty options.

- Be realistic about returns. Genuinely safe products pay close to the risk-free rate; if a "guaranteed" product promises far more, verify it against the MAS Investor Alert List first.

- Review and rebalance as rates and your goals change — in a falling-rate environment, locking in longer tenors can be worthwhile.

The safest strategy combines several instruments to balance guaranteed returns, liquidity and time horizon. For higher-growth options across the full risk spectrum, see our guide to the best investments in Singapore.

Sources

- Monetary Authority of Singapore (MAS) — SSB, T-bill and SGS rates, auctions, and the Investor Alert List: www.mas.gov.sg

- Central Provident Fund Board (CPFB) — CPF interest rates, Special Account closure, cash top-up tax relief and the Matched Retirement Savings Scheme: www.cpf.gov.sg

- Singapore Deposit Insurance Corporation (SDIC) — deposit insurance coverage and scheme members: www.sdic.org.sg

- Bank and provider websites — fixed deposit and savings-account rates (DBS, OCBC, UOB) and the Singlife Account, as of June 2026.

- Kilde — platform statistics: www.kilde.sg/statistics

Disclaimer Notice

This page is provided for general informational purposes only and does not constitute legal, financial, or investment advice. Please refer to our Full Disclaimer for important details regarding eligibility, risks, and the limited scope of our services.

FAQ

Singapore Government Securities — SGS bonds, Singapore Savings Bonds (SSBs) and Treasury Bills (T-bills) — are the safest, backed by the AAA-rated Singapore government with virtually no default risk. SDIC-insured fixed deposits and CPF are also considered very safe.

A common guideline is 20–30%, rising as you approach retirement or have near-term goals. The right figure depends on your own goals, risk tolerance and time horizon.

If you hold to maturity, you receive your full principal back. The only way to lose money is selling on the secondary market before maturity when prices have fallen (for example, after interest rates rise).

It depends on your horizon. For flexibility, the SSB (2.11% 10-year average, redeemable any month) is hard to beat. For locking in a fixed rate, the best fixed deposits and 6-month T-bills both sit around 1.5%. For everyday cash, a high-yield savings account can pay more if you meet the conditions.

SSBs, SGS bonds and T-bills (held to maturity), SDIC-insured deposits, CPF, and many endowment and insurance savings plans return your principal in full. Note that some plans guarantee capital but not the interest rate.

For a truly fixed, guaranteed return, fixed deposits and SGS coupons are the clearest options, alongside CPF's guaranteed interest. Returns are modest (roughly 1–4% depending on the product and tenure), which is the trade-off for certainty.

Foreigners can invest in T-bills, SGS bonds and even SSBs (open to any individual aged 18+ with a local bank and CDP account), and can place fixed deposits and use most savings accounts. CPF is for citizens and PRs only, and some endowment plans are restricted to residents — check eligibility per product.

Six-month T-bills, short-tenor fixed deposits, the redeemable SSB, money market funds and cash management accounts are all suited to short horizons, currently yielding roughly 1.3–2.1% p.a.

SGS bonds pay coupons every six months, SSBs pay interest twice a year, high-yield savings and the Singlife Account credit interest monthly, and some endowment and annuity-style plans provide regular payouts. Fixed deposits and T-bills typically pay at maturity instead.